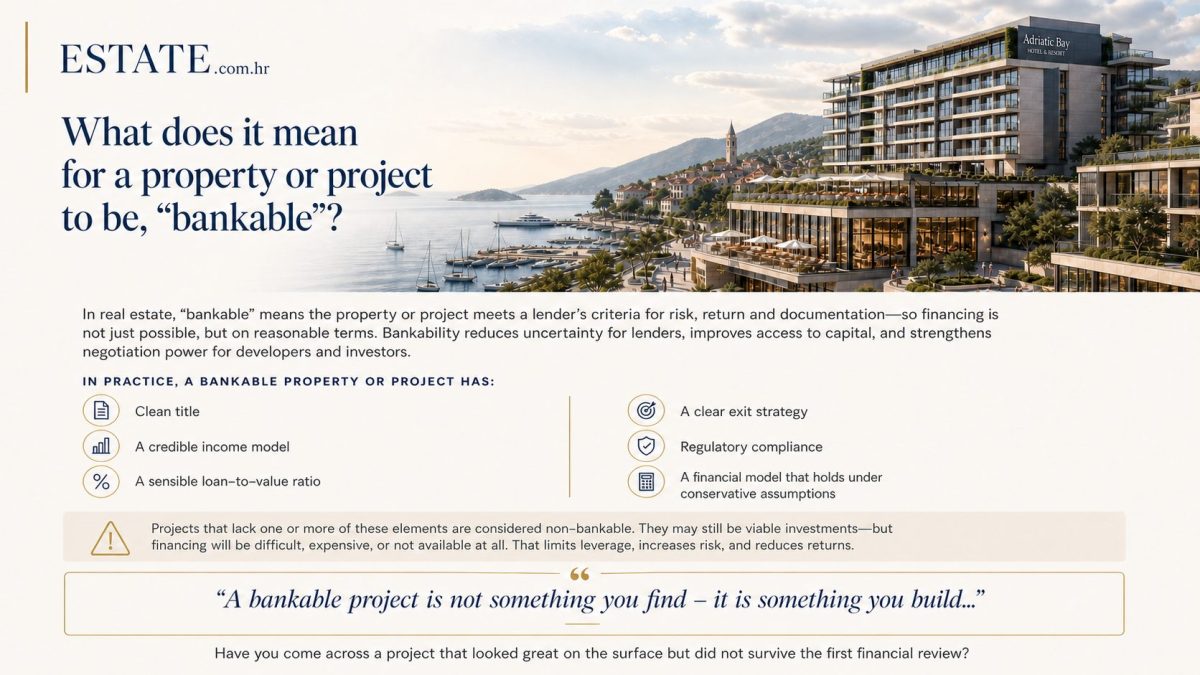

What a Bankable Project Actually Looks Like

In practice, a bankable property or project has all of the following:

Clean title

No encumbrances, disputes, unresolved inheritance situations or unclear co-ownership structures. This sounds basic, but a significant share of Adriatic properties – particularly older villas, agricultural land converted for development, and family-owned coastal parcels – carry unresolved legal issues that immediately disqualify them from institutional financing. One unclear co-owner, one unregistered building, one unresolved estate can stop a transaction worth millions of euros at the due diligence stage.

A credible income model

Revenues that can be documented, projected and defended in front of banks or investors. For hospitality assets this means real ADR, occupancy and RevPAR data – not aspirational figures based on what the best hotels in Dubrovnik charge in August. For residential it means documented rental income, lease agreements or realistic absorption assumptions. The model needs to work in a normal year, not just in a record tourism summer.

A sensible loan-to-value ratio

LTV that a bank can accept without special conditions or personal guarantees that undermine the whole structure. In the current credit environment in Croatia, this typically means conservative valuations and a clear understanding of what the bank’s own appraiser will produce – which is often materially different from the owner’s asking price.

A clear exit strategy

Who are the likely buyers, at what price, within what timeframe, and with what realistic days-on-market assumptions? Serious capital does not enter a project without a credible path out of it. This includes understanding the current liquidity tiers in the market – whether the asset, once developed or repositioned, will trade in the sub-90-day segment or risk sitting for 180+ days.

Full regulatory compliance

Building permit, occupancy permit, compliant spatial plan, energy certificate, coastal zone compliance where applicable. This is especially critical on the Adriatic, where spatial plans vary significantly between municipalities, where coastal building regulations are strict and where permits can take years. A project with a partially issued permit or one that relies on a future spatial plan amendment is not bankable – it is speculative.

A financial model that holds under conservative assumptions

Not just in the best-case scenario. Any experienced investor stress-tests a model against lower occupancy, higher construction costs, longer sales periods and rising interest rates. A bankable project survives those scenarios with an acceptable – not just theoretical – return. If the numbers only work if everything goes perfectly, the project is not bankable; it is optimistic.

The Other Side of the Equation

The opposite of a bankable project is what is appearing all over the Adriatic right now: a beautiful property, an attractive location, a compelling story – but missing documentation, inflated income assumptions, an unresolved inheritance dispute, or a building permit still not issued after years of trying.

These properties may eventually find a retail buyer willing to overlook the issues or take on the risk personally. But they will not find serious institutional or professional capital. And that is exactly why they sit on the market for 180, 300 or 500+ days – accumulating carrying costs, losing the best windows of buyer interest, and often eventually selling at a lower price than they could have achieved had they been properly prepared from the start.

Bankable Is Built, Not Found

This is perhaps the most important insight: a bankable project is not something you find – it is something you build. For a land owner or developer, this often means investing 6–18 months of preparation work before approaching the market: resolving legal issues, obtaining planning documentation, commissioning a credible feasibility study, preparing a professional information memorandum and building the financial model that a bank or investor can actually underwrite.

That preparation is not a cost – it is the difference between attracting serious capital at a serious price and circulating on portals indefinitely.

For investors considering an acquisition, the same logic applies in reverse: the due diligence question is not “do we like this asset?” but “can we make this bankable, and at what cost and timeline?” Sometimes the answer is yes, and the gap between current price and bankable-adjusted price creates the investment opportunity. Sometimes the answer is no – and that is equally valuable to know before committing capital.

If you are preparing a property or project for the Croatian or wider Adriatic market and want an independent review of its bankability – title, regulatory status, income model, financial structure and exit strategy – we would be happy to have a confidential conversation.

estate.com.hr